A few days ago, some readers wrote emails tellingAmerican Life Insurance GuideEditor of "I feel that your industry is serving very wealthy customers. I don’t know if there is any way to help middle-class families like us.. '

At the same time, in the life experience of the life insurance guide community editors, whether in social media or in the WeChat circle of friends, financial and insurance marketing information for "high net worth individuals" will frequently appear every day; traditional radio or Financial and insurance advertisements such as "Wealth Inheritance" in the newspaper media also frequently cover the Chinese community. A reader from the San Francisco area told the American Life Insurance Guide. "There are life insurance advertisements on the radio every day"— —Under the long-term influence of this marketing atmosphere, it is easy for us to automatically associate "life insurance" with "wealth" and "rich people" and other keywords, and produce "life insurance seems to have nothing to do with ordinary people." Wealthy people will buy life insurance" subjective feelings, and take the initiative to "keep away."But is this true?

American Life Insurance GuideOfinsurGuru©️Life Insurance AcademyColumn, let’s share some views on this point of view today.

1. "The rich" may not need a life insurance policy

OnAmerican Life Insurance GuideOfinsurGuru©️Life Insurance Academy Lecture 2 "Do i need life insurance"In this article, we analyzed the groups that may need life insurance. Among them, "Rich man"The demand for life insurance is ranked last.

From a financial point of view, the real "wealthy people" can already complete self-protection financially. When they encounter some "losses", they can bear the corresponding financial problems themselves.In other words,A problem that can be solved with money is usually not a problem.Therefore, their demand for life insurance functions whose functional nature is "Indemnity" is not so urgent.

The life insurance policy tool, for this type of group, is more used forAsset protection.After reaching a certain age, due to the American social system (tax laws, inheritance certification, etc.), it is natural to consider using the life insurance policy tool.

2. The most in need of protection is ordinary American families

According to a report by the Pew Research Center in 2019, the annual household income $40,500 To$122,000 In between, even a middle-class family.

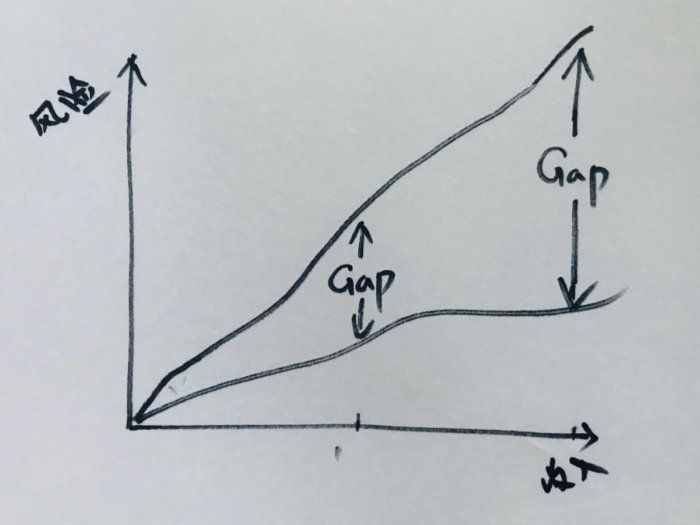

As the main class of society, we face thisHousing, medical care, education, and retirementAnd many other issues.These problems, as the government, have only given a guarantee plan. If you pursue an "Above Bottom Line" life, you will need to spend extra money to solve them.

In the past 30 years, the increase in income of ordinary American households has lagged completely behind the increase in housing, medical care, education, and pensions, while the debt ratio has gradually increased with rising prices and consumption.

In the past 30 years, the increase in income of ordinary American households has lagged completely behind the increase in housing, medical care, education, and pensions, while the debt ratio has gradually increased with rising prices and consumption.

Although the middle-class group in the United States, the proportion of the national population has been maintained at 52%1About the ratio.However, compared with the past, on the one hand, ordinary families have more debts and need to cover more risks. On the other hand, faced with failed income growth and insufficient income to pay for family life, the couple works full-time with one family member. Doing multiple jobs has gradually become the norm.As a recent cover report of Fortune magazine pointed out: "The middle class is shrinking2. "

In this process of social development, the gap between the risk and income faced by every ordinary family has gradually expanded——The normal rate of labor expenditure and income return is simply not enough to fill this growing financial gap (Gap)—— It even exceeds the scope of leverage protection provided by the old financial insurance products (non-consumer).

The development of the industry always matches the evolution of society.In the field of financial insurance, when the old products are insufficient to make up for the needs of the new situation, new financial insurance tools are bound to evolve to cover family risks, while providing higher leverage to bridge the growing gap area.

Instead, the first point mentioned above is printed here-there is almost no Gap range for "rich people", so the demand for financial insurance protection is not high at all.

Therefore, there is a real urgent need for life insurance products, not "the rich",It's a vast ordinary Chinese family.

3. "Life Insurance" is not an insurance, but a financial instrument

American Life Insurance GuideThe brokers in the community found in actual work observations that most consumers have a deep-rooted traditional impression of the word "insurance".Especially younger individuals or families usually feel that "life insurance is not necessary" and that "purchasing personal life insurance may be very expensive", so they actively choose to push the tool of "life insurance" far away from them.

However, many life insurance products in the U.S. market already belong toFinancial product.Instead of traditional consumer “insurance” products.It is aThe name contains the word "insurance"The financial tools that can help us manage the comprehensive risks brought about by social development.

In the context of cognitive asymmetry, many young Chinese individuals or families, from the very first moment, subjectively chose to give up the "biggest advantage" of holding this financial instrument.

The reason for saying this is that from common sense, the most valuable thing in a person's life is "time."The earlier financial and insurance planning is carried out, the more "time" costs are paid, the less money costs are paid, and the more long-term protection is exchanged.This is also determined by the nature of such financial insurance products.

The reality is that it is often when people reach middle-aged and old age, with the development of their careers, they begin to face the rules of the game in a deeper level of the social system, and with the experience of life, they begin to think seriously about managing the risks of family members. At this time, they begin to take the initiative. Look for "tools" you can use.At that time, when turning to this tool again, because there is no cost support for the most valuable "time", it is usually necessary to pay a high cost to fight against the gap that has expanded over time, and the guarantee of exchange, in contrast, is usually not As expected.

Article summary

From this article, we shared about "It is not the "rich people" who need life insurance the most, but ordinary families like us"This view.For each of our ordinary Chinese families, what we have to do is not to fight against the inflation of daily necessities, but to use various tools provided by the American financial system to manage the huge gap between risk and income, which is the biggest increase in health care and education. Spend more reserves and face the financial needs of retirement.

Under the rules of the American social system, life insurance policies are a widely used financial tool, rather than a traditional "insurance" product, to help face these problems.Planning and selecting products as early as possible can use "time" to greatly reduce risk management costs, and in exchange for more long-term protection.

At last,Reasonable selection and designThe life insurance policy of China is actually not expensive, and may even be cheaper than expected.More importantly, mastering this financial tool can give full play to the "time" advantage and manage the comprehensive risks brought about by social development. At the same time, it can also help every family form the habit of long-term savings and financial management. This is also American life insurance. The guide network shares the purpose of this article.

American Life Insurance Guide CommunityMost of the licensed Chinese-language brokers here come from ordinary Chinese families. Like everyone else, we will face the problem of how to deal with these risks brought about by social development.

While empathizing, we hope to use our experience and professional knowledge to help readers of different ages through sharing, eliminate cognitive misunderstandings, and establish a family risk management mechanism as soon as possible.If you need our help, please scan the QR code at the bottom of the page orE-MailContact to make an appointment assessment.

(>>>Related reading: Evaluation|What lessons have been learned from the insurance policy accounts of New York State policyholders that have been deposited for 14 years?)

(>>>Related reading:Evaluation|The difference of $186 million in income, the same insured, professional design plan VS general plan )

(American Life Insurance Guide website insurGuru©️Life Insurance Column)

appendix:

01."The American middle class is stable in size, but losing ground financially to upper-income families", 09.06.2018, Pew Research Center, https://pewrsr.ch/2U9aaCC

02."The Shrinking Middle Class", 12.20.2018, "Fortune Magazine", https://bit.ly/2GTyxLO