ApplyingSavings Participating Whole Life Insurance(Whole Life), the policyholder needsChoose options for how to use policy dividends.Some of the most common dividend options (Dividend Option) are:

- Purchase Paid-Up Additions (PUA)

- Cash withdrawal

- Reduce future premiums

- ...

in the text,American Life Insurance GuideWill introduce,Savings Participating PolicyOne of the most commonly used dividend options in the policy is to use the dividend amount of the policy to purchase additional protection and help the accumulation of the cash value of the policy, that isPaid-Up Additions (PUA)this way.

What is Paid-Up Additions/PUA?

Paid-up additions in the Whole Life policy, PUA for short, are the policyholders who use the dividends in the policy to purchase additional protection.We can understand this approach as that the policyholder uses the dividend amount and purchases a lot of "small insurance policies."

These "small insurance policies" are alsoSavings Participating Policy, So you will also enjoy dividends, and the accumulation of cash value will also accumulate according to time compound interest calculations.Because these "small insurance policies" are constantly being purchased, the death compensation and various pre-mortem benefits of the insured will also increase.Policy holders can also surrender part of these PUAs, or borrow the part of the PUA.

When applying for insurance, you need to make a choice.

How does Paid-Up Additions/PUA work?

When you choose the policy dividend to purchase additional protection in the form of PUA when you apply for insurance, the cash value of the PUA part will increase over time. These increases are to enjoy tax deferred benefits.

Another advantage of PUA is that the death benefit of the insurance policy has been increased, and the insured gets more protection, and there is no need for additional underwriting medical examinations and re-underwriting.

This is very beneficial to the insurance policy when the health condition is far worse than when you first bought the insurance policy as you age.For this type of policyholder, in the case of advanced age and poor physical health, the cost is no longer the primary consideration. Insurance companies are no longer willing to underwrite, which is the biggest problem they will face.

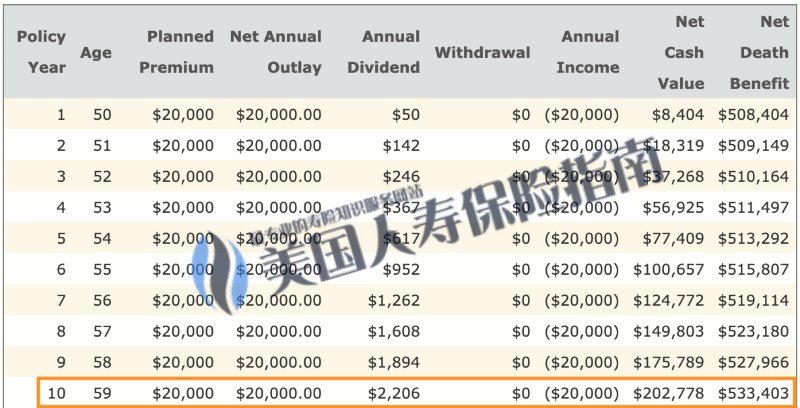

Policy comparison

Article summary

Paid-Up Additions Option is usually automatically integrated inSavings and dividend life insurance policies(Whole Life).There are also some insurance companiesadditional terms(Rider), and allows you to add it after you have purchased the insurance.Different savings and dividend products of different insurance companies may have different names for this option, and the specific functions may be different from those described in the text.Before deciding to apply for insurance, please contact professional insurance policy design practitioners or financial planners for detailed understanding.

Key function description

- Paid-up additions (PUA) are dividends provided by policyholders using savings-participating insurance policies, and additional savings and dividend insurance protection purchased.

- Paid-up additions (PUA) itself can enjoy dividends, and the cash value of this part can grow compounded over time.

- The policyholder can surrender the Paid-up additions (PUA) to get back the cash value, or borrow this part.