When comparing the policy account products of different asset-management insurance companies, customers usually discuss with insurance consultants in the American Life Insurance Guide community,"This product does not seem to be highly competitive", "The return on investment of that insurance company does not seem to be high"Wait for questions.So it came out naturally,What exactly is the "competitiveness" of American insurance asset management? What medium do we rely on to bring the value of "return rate" into our minds?Is this value representing "competitiveness" reliable?What should we care about?

How did the "competitiveness" of the asset management of the insurance policy come from?

Insurance companies usually use the insurance premium fund pool accumulated by policyholders to make profits. The principle of this profitability is shown in the chart "Rejected insurance, increased premiums and suspended sales, the insurance window for the new crown epidemic in the United States is closingA detailed description is given in the article.

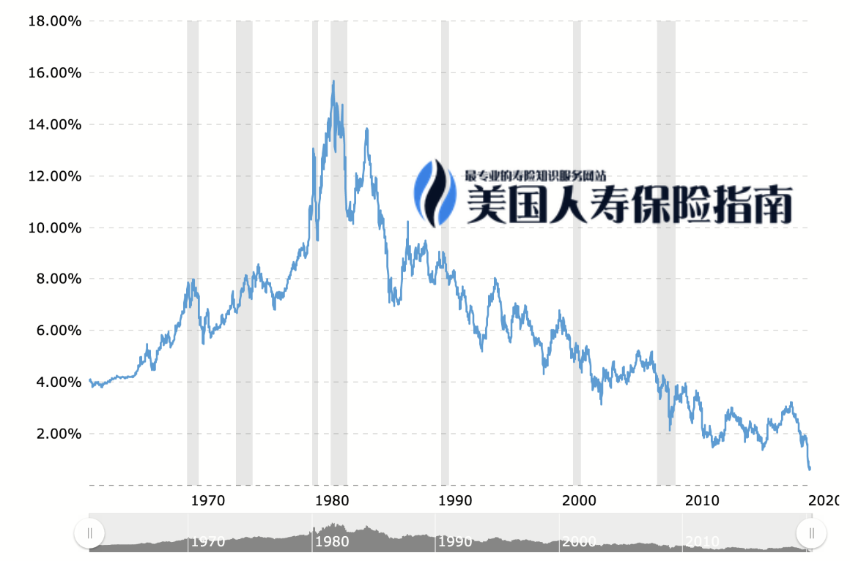

(Since 1980, interest rates have been falling for 40 consecutive years)

(Since 1980, interest rates have been falling for 40 consecutive years)

Due to long-term low interest rates, traditional insurance product types and previous businesses can no longer help insurance companies make money. The American Life Insurance Guide has also reported on several insurance companies in the past two years.Insurance company exitOrResellNews about the personal life insurance business.

In this case, some insurance companies have begun to graduallyasset Management"The direction of this concept is transformed. Then, the investment type,Index insuranceProducts began to emerge in the market after 2000, and rose rapidly in just 20 years, gradually occupying the mainstream market for personal life insurance in the United States.

Until now, "Insurance financingThe concept of "buying insurance" is beginning to spread, just like buying stocks or buying funds, it has become a part of the daily financial management of many of us.

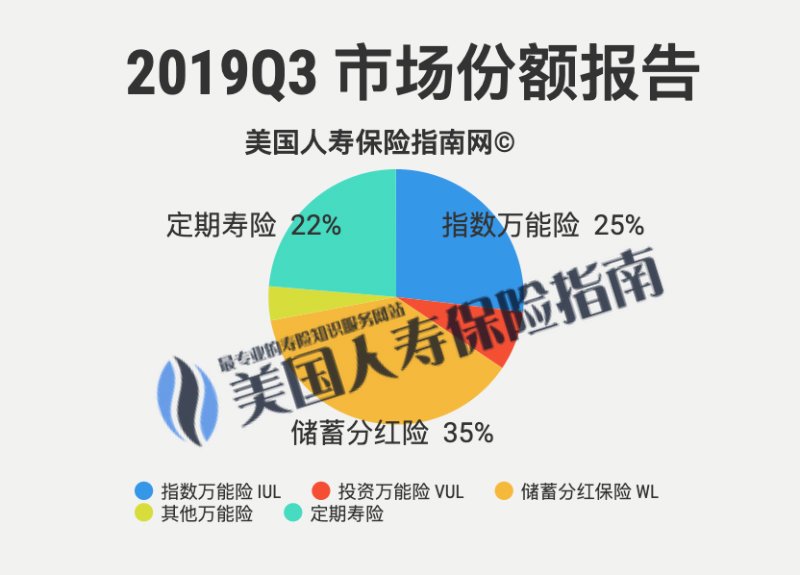

More like the "Passive Management" attributeIndex products, The traditional advantages of compound overlay "insurance" provide a powerful risk management tool and cornerstone for the accumulation of family wealth.Therefore, index products have a highermarket share.

What is the ideal "competitiveness"?

以First appearedOfIndex insuranceTake the product as an example,Regardless of brand premium,如果The cost of the policy, against the underlying market indexAllExactly the sameIdeal situation, Then, who gave itRevenue CapThe higher the value, the more generous the insurance company is in distributing dividends and transferring profits to policyholders.

This situation often means that the corresponding insurance productsThe numerical value on the plan is more beautiful——It shows that under the same market trend in the future, this insurance company will get more cash value benefits than other insurance products.therefore,The stronger the competitiveness in the moment.

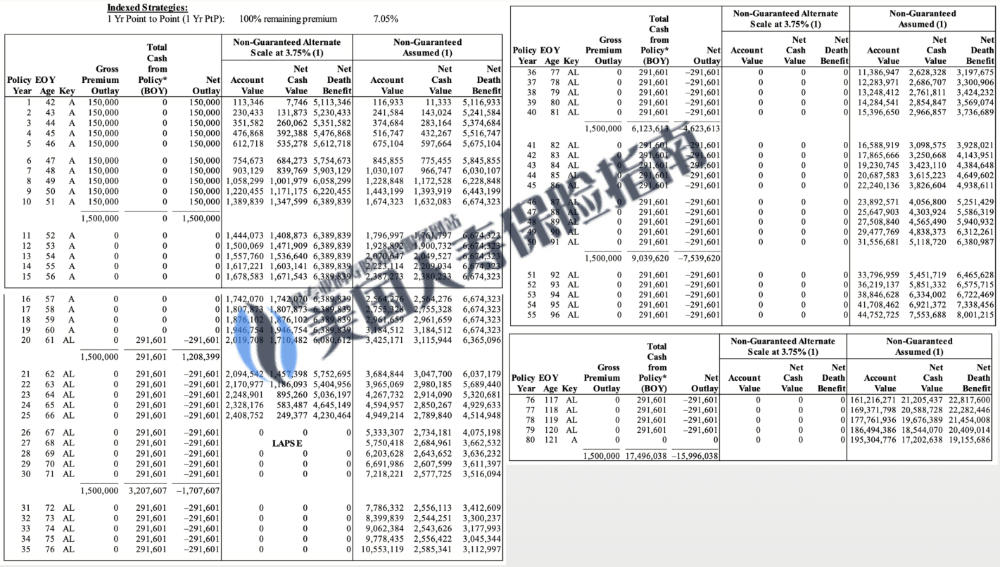

(Example: Demonstration of "Scheme Suggestion Form" of an insurance company with high cap. This picture does not constitute a recommendation for insurance, nor is it a guaranteed result)

(Example: Demonstration of "Scheme Suggestion Form" of an insurance company with high cap. This picture does not constitute a recommendation for insurance, nor is it a guaranteed result)

Although this is the truth, in the real world,There is no such simple judgment criterion and ideal contrast environment.This is because every excellent insurance company has a different professional market area, and there are so many differences in policy costing and welfare protection, there is no standard that can be used to make a completely fair comparison.

In addition, with the competition and development of the market, index insurance products have been upgraded from the first generation to the second generation. The two coexist in the market and there are obvious product differences.The more beautiful values in the latter plan can be calculated in a completely different way, directly bypassing the "Cap revenue Cap"Determinism.

What is "competitiveness" not

However, many marketing and gimmicks have drawn our attention to the "number" in the policy design.However, "number" is never neutral.Insurance companies know this better, and they have also worked hard on the calculation system for display.

Back 5 years ago, the China Insurance Regulatory Commission’s AG49 regulations had not been formally introduced-taking a V insurance company, a popular Chinese wealth management market at the time, as an example, the planning plan of its insurance policy account, or the figures on the product plan, can be done Let the younger generations stunned.

If you only look at the numbers, this is definitely a "competitive" product.

But after many years, it was not the customer or the insured who felt the hardship first, but some practitioners who also believed that this was a "competitive" product at the time and followed to sign.

After the executives of the original insurance group were fired, they turned to another financial group, re-operated and established the life insurance business, and bought the "company history" through acquisitions.Reappeared with a new name and really beautiful numerical plan display table——Think more deeply, will this kind of operation of large capital market bring about the same market reincarnation again?As industry observers, we have always been skeptical of this type of insurance company.

Finally, from a professional point of view,The policy plan has always been just a reference.From the moment the policy is signed into effect, no policy account will automatically operate in exactly the way expected by the plan.如果onlyIt may be debatable to judge whether a product is "competitive" based on the reference value on a reference template that has no legal effect, and to make a financial decision.

(>>>Recommended reading:Professional Post|What is the American Life Insurance Recommendation (Illustration)?What are the controversies and highlights? )

This is why we emphasize,After the policy takes effect, the management of this type of policy account for up to 10 years, 20 years,Does the insurance company provide more management tools and options for cash withdrawal,The specificity of the overall business of the insurance company and the nature of the management team,It may be more important than paying attention to the importance of the value display in the design of the insurance policy. This is the basis for truly reflecting the "long-term average rate of return of the insurance policy".

In the next column, we will continue to share several important rules for applying for a savings participating insurance account & IUL index insurance policy account in 2020.

1. How to judge whether this insurance company is reliable or not?

2. Why do you choose insurance consultants and brokers instead of insurance companies?

3. Be clear about what you want, or what you don't want.

4. How can I take money out of the insurance policy?What are the options and the corresponding costs?

(>>>Recommended reading:2018 golden rules for buying IUL index insurance in 4 )